Savings Feature

Planyour

You have the flexibility to start, change or stop your savings contributions; or make a lump-sum contribution at any time during the year. Interest on your GUL savings contributions grow tax-deferred,1 which means the value of your savings has the potential to grow more over time.

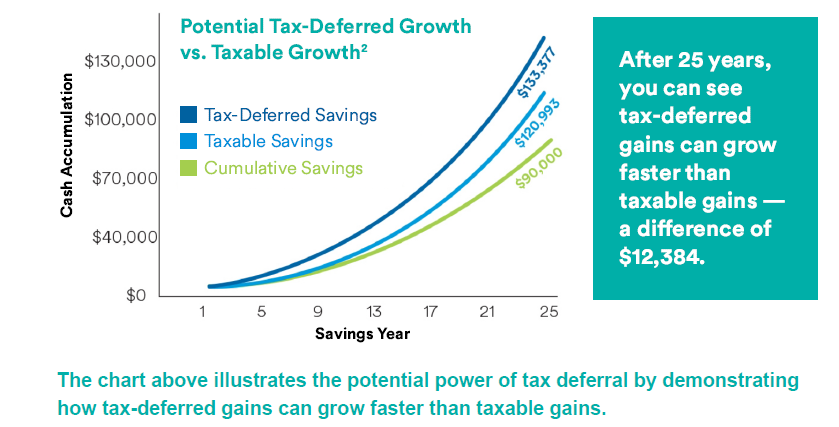

The power of tax deferral2

This example assumes a savings of $300 per month ($3,600 per year), a 3% yearly return over a 25-year period, and no withdrawals from cash value.

The bottom green line shows money saved over time. The light blue line in the middle shows potential growth if the savings was taxed each year at a 24% federal tax rate. The top dark blue line shows the growth of the savings, if tax-deferred.

See for yourself how tax deferral works.

Understanding the GUL tax-deferred savings feature1

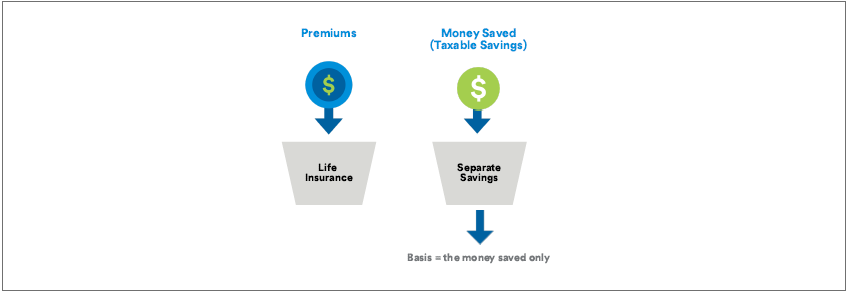

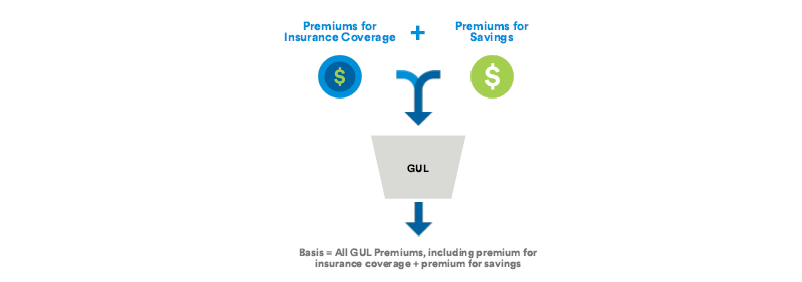

The illustration below represents how GUL turns the cost of life insurance, an expense, into a potential tax savings.1 Let’s examine two scenarios that satisfy the same needs: financial protection and savings.

Purchasing life insurance while saving separately.

All potential gains from the money saved are subject to tax. The life insurance premium is an expense only.

Plan ahead

Make an informed decision and view a short video on the benefits of GUL coverage from MetLife.

Enroll or update coverage

To speak with a GUL Benefits Specialist, call 800-756-0124,

Monday - Friday, 8 a.m - 8 p.m EST

1 Earnings within your GUL coverage grow income tax-free while the policy stays in force. Please consider your time horizon, tax rates, and the effect of fees and expenses, including any premium expense charge, when evaluating the benefit of GUL tax deferral. See your Certificate for complete information.

2 The illustration is used only for the purpose of demonstrating how tax-deferred gains can grow faster than taxable gains. It is not intended to, nor does it represent, any growth that may occur in the GUL savings portfolios. Insurance company asset charges, administrative fees and premium expense charges have not been deducted. The cost of insurance charges, which vary with each individual certificate, has not been deducted. Deduction of these charges would result in lower returns. The tax rate used in this chart is a hypothetical tax rate. Actual rates will vary.

3 In general, participants may withdraw cash value equal to premiums paid without tax consequences. However, if the funding of the certificate exceeds certain limits, it will become a “modified endowment contract” (MEC) and become subject to “earnings first” taxation on withdrawals and loans. An additional 10% penalty for withdrawals and loans taken before age 59½ will also generally apply to MECs. We will notify you if a contribution would cause your certificate to become a MEC. Withdrawals and loans will reduce the death benefit and cash value and thereby diminish the ability of the cash value to serve as a source offunding for cost of insurance charges, which increase as you age. Withdrawals are subject to an administrative fee of 2% of the amount withdrawn, not toexceed $25. Outstanding loan amounts do not participate in the interest credited to the interest-bearing account and can have a permanent effect on certificate values and benefits. Upon surrender, lapse, or case termination, including those circumstances where termination of the group contract results intermination of individual certificates/policies, loans become withdrawals and may become taxable to the certificate owner.

Any discussion of taxes is for general informational purposes only and does not purport to be complete or cover every situation. MetLife, its agents and representatives may not give legal, tax or accounting advice and this document should not be construed as such. Please confer with their qualified legal, tax and accounting advisors as appropriate.

Nothing in these materials is intended to be advice for a particular situation or individual. Please consult with your own advisors for such advice. Like most insurance policies, MetLife GUL contains exclusions, limitations and terms for keeping it in force. MetLife can provide you with costs and complete details.

Group Universal Life insurance (GUL) is issued by Metropolitan Life Insurance Company (MLIC), New York, NY 10166, and distributed by MetLife Investors Distribution Company (MLIDC) (member FINRA). MLIC and MLIDC are MetLife companies. Certificate Form 30025 (1/95) As amended by form 3E59 (5/2005).