MetLife Retirement & Income Solutions

Defined Contribution Plan Design: Facilitating Income Replacement In Retirement

Feb 23, 2024

MetLife Retirement & Income Solutions

For plan sponsors, facilitating the ability of defined contribution (DC) plan participants to generate income for retirement from the plan may be as important as any program enhancement they make. That’s because one of the toughest challenges for a DC plan participant is figuring out how to turn their retirement savings into income they can’t outlive.

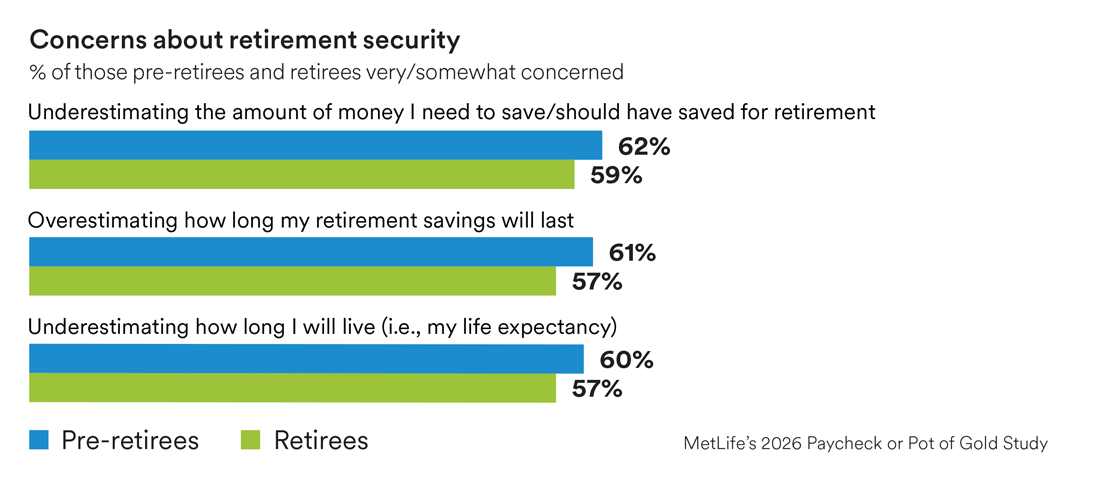

According to MetLife’s research, pre-retirees and retirees fear they may not have properly planned for the sustainability of their retirement funds, and they are concerned about their retirement security.1

An important consideration for DC plan sponsors is determining whether or not retirement income solutions should be considered as a component of a DC plan and, if so, in what way. Plan sponsors contemplating the decumulation stage should answer the following questions for their organizations:

If the answer to any of these questions is “yes” or even “maybe”, then it may be prudent for you to consider adding a guaranteed income form of benefit payment to your company’s DC plan.

Evaluating retirement income approaches

A participant’s individual needs in retirement, including expected living and health expenses in retirement, and the amount of income they need to replace in retirement, will likely dictate, to a large extent, their interest in any retirement income features added to the plan. MetLife’s research shows that nine in 10 retirees (92%) and pre-retirees (86%) say a retirement “paycheck” is very important or absolutely essential to pay their bills.1 An evaluation of the various ways in which a retirement income benefit can be offered as a component of a DC plan today includes:

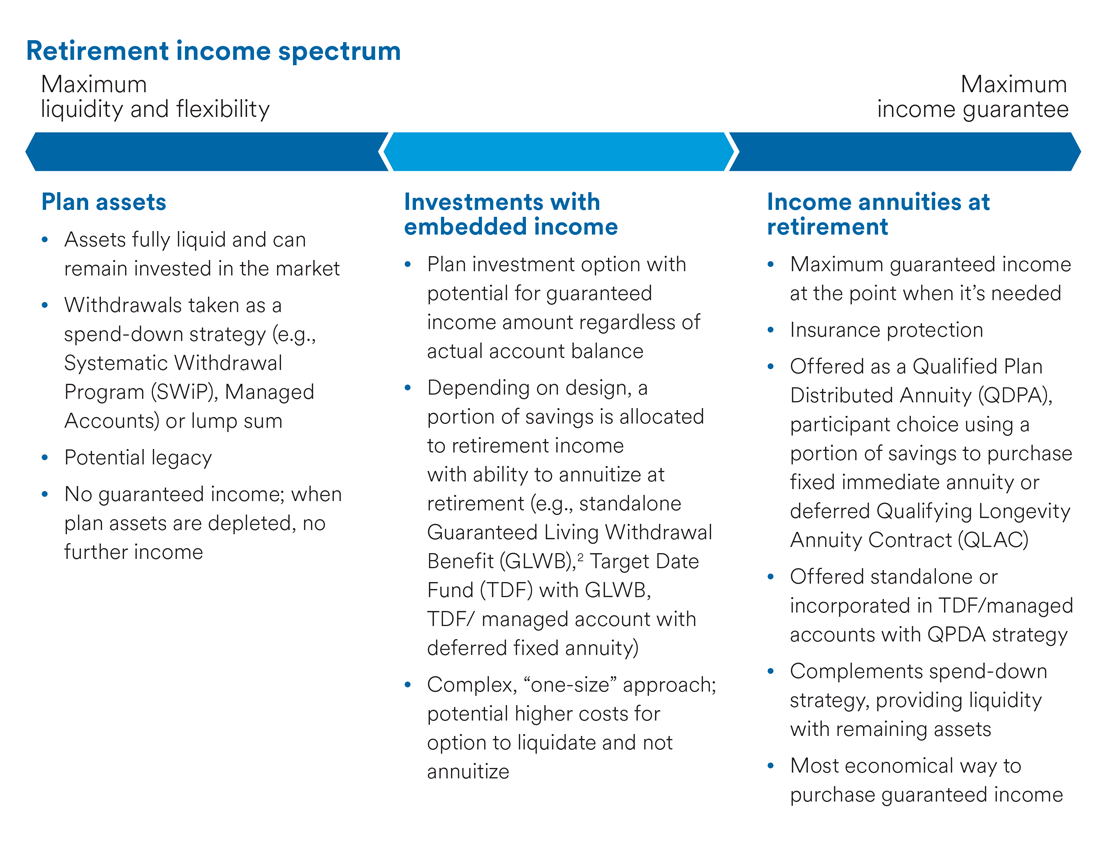

It may be helpful to think of each type of retirement income option available today as a spectrum that ranges from maximum income flexibility to maximum income guarantees. On this spectrum, for example, a systematic withdrawal plan would be at one end of the spectrum and an immediateor deferred fixed income annuity would be at the other end.

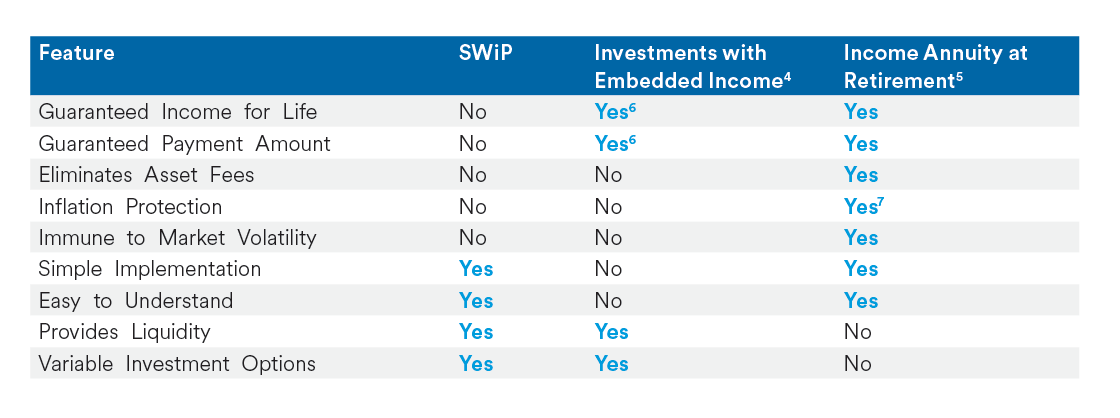

“Systematic withdrawal” plan (SWiP) approach

“Systematic withdrawal” programs (SWiPs) were the retirement industry’s initial attempt to introduce some form of structure or planning into the DC distribution process, but a closer look suggests that a SWiP approach, particularly if it is the only approach provided in the plan, can be problematic for a number of reasons, including the following:

Navigating complexity and innovation: investments with embedded income

In recent years, the qualified retirement plan industry has seen the emergence of many new products along the retirement income spectrum as providers seek to find features and positioning that will meet emerging plan needs and participant preferences. At the same time, this competition and innovation around retirement income solutions has the potential to create significant confusion for both sponsors and participants.

Sponsors may be well-advised to first clearly establish the outcome they want to achieve, which they should keep in mind as a guiding principle for plan design considerations. Plan sponsors may also want to consider adopting a “Retirement Income Policy Statement,” which would outline the retirement income options available to their participants. This could be similar to the now widely used “Investment Policy Statement,” which most plan sponsors use as a guideline for their investments. Determining which type of solution to offer should come after the decision has been made to re-establish the DC plan as a retirement plan whose intent is to help participants generate retirement income.

One area of experimentation, first in retail and more recently in the institutional retirement arena, is a product category that we refer to as investments with embedded income. These are plan investment options for participants contributing during their working years, which have the potential for guaranteed income. Often offered as a Qualified Default Investment Alternative (QDIA), these options tend to be complex. Depending on design, a portion of savings is allocated to retirement income with the ability to annuitize at retirement (e.g., standalone Guaranteed Living Withdrawal Benefit (GLWB), Target Date Fund (TDF) with GLWB, TDF/managed account with deferred fixed annuity). However, if the participant decides not to avail themselves of guaranteed income, they presumably are paying potentially higher costs for the option to liquidate. Rather than being tailored to the needs at the plan participant at the point of retirement, investments with embedded income take a “one-size-fits-most” approach.

Providing income with fixed income annuities

Deferred and immediate income annuities provide individuals with an income stream that cannot be outlived — period. This type of guarantee can only be achieved with an annuity. An annuity should be considered to fill any gap that exists between the level of fixed living expenses and the amount of guaranteed income provided by sources such as Social Security or a monthly pension payment.

Annuities, like all insurance products, work on the concept of pooling risks which, in the case of retirees, include longevity, investment and inflation risks. The pooling of risk is not new to most people. For generations, Americans have held the majority of their retirement assets in a risk pool. Social Security and corporate pension plans are both examples of mortality pools. When an insurer pools longevity risk for a large group of retirees, money that is left over from people who die earlier than the average life expectancy is used to continue to pay people who outlive the average age. Pooling works because everyone shares a common risk, and while it can be accurately predicted how many people will be adversely affected by the risk, it is not possible to know in advance which specific individuals they will be.

Since an income annuity is an insurance product, it should not be considered an investment alternative but a complement to other sources of retirement funding. Mutual funds and other investments play an essential role in retirement as they provide liquidity and possible asset growth that can help offset inflation. However, as well as being vulnerable to market volatility, the income they provide may run out if one lives longer in retirement than anticipated. By allowing plan participants to place part of their retirement savings in a fixed income annuity, they will be able to generate income that lasts a lifetime, manage their remaining assets more efficiently, and maximize and protect their future income.

The value of keeping it simple for plan participants

For a sponsor wishing to provide guaranteed lifetime income from a DC plan, it is in the best interests of plan participants to keep it simple. While it may be tempting for plan sponsors to believe they should alleviate potential participant objections by offering products with many features, simplicity may be a more effective guiding principle for the decision-making process. This is important because participant behavior has consistently shown that complexity, such as too many choices and features, often leads to participant inertia (i.e., avoiding taking any action).8 For this reason, beginning with a “back-to-basics” approach when considering guaranteed retirement income options may be the most constructive strategy.

As a final consideration, the emerging wealth of behavioral research suggests that how a decision is framed — e.g., the way in which it is perceived by participants — may be the most significant determinant of its outcomes. For example, “life annuities are more attractive when presented in a consumption frame rather than an investment frame,”9 meaning that individuals are more likely to recognize the benefits of a guaranteed stream of income when the focus is on the purchasing power this income stream can provide, rather than on risk and return features, such as principal guarantees.

Plan sponsors play a critical role in the ultimate retirement outcome for millions of American workers. While encouraging retirement plan savings is incredibly important, that’s only one piece of the workplace retirement equation. Plan sponsors should also design retirement plans that help ensure successful retirement outcomes for the plan participant. By expanding access to guaranteed lifetime income solutions, employers can empower plan participants to confidently transition into retirement —and help ensure their retirement savings lasts.