MetLife Retirement & Income Solutions

How to Evaluate Stable Value Funds: 4 Tips for Plan Sponsors and Advisors

Jul 28, 2023

MetLife Retirement & Income Solutions

Stable value funds can be ideal for plan sponsors or plan advisors who need a capital preservation option in the defined contribution (DC) plan line-up since it is the only capital preservation option designed specifically for qualified retirement plans.

Let’s look at the fundamentals of a stable value fund, as well as four criteria plan sponsors and advisors should evaluate to ensure the fund they select is the right fit for their plan.

What’s a stable value fund?

Stable value funds are capital preservation vehicles that invest in a diversified mix of conservative fixed-income investments — primarily high-quality bonds with strong credit ratings. This allows the funds to deliver steady and predictable returns in all market cycles.

According to MetLife Stable Value Sales Director Matt Curtin, the role of a stable value fund within a DC plan is two-fold:

“A stable value fund provides a guaranteed return to the plan participant regardless of the market conditions they’re investing in,” says Curtin.

When does stable value make sense for a defined contribution plan?

Stable value funds provide safety and security to a DC plan no matter the age of the plan participants. Because plan sponsors and advisors need to provide a wide range of options to accommodate participants’ life stages, risk tolerances, and time horizons — including those nearing or in retirement — stable value funds can be a steadying addition to a DC plan line-up.

“Stable value can offer some stability for those who don’t want to be exposed to market risk, and also want a secure retirement,” says Curtin.

Stable value funds use an insurance “wrapper” that helps protect against losses. Wrap providers like MetLife smooth the volatility of the underlying bond portfolios through the issuance of an insurance contract (wrap), which allows the funds to use the book value (or contract value) of their underlying holdings and maintain a stable share price even if the market value of the bond holdings declines.

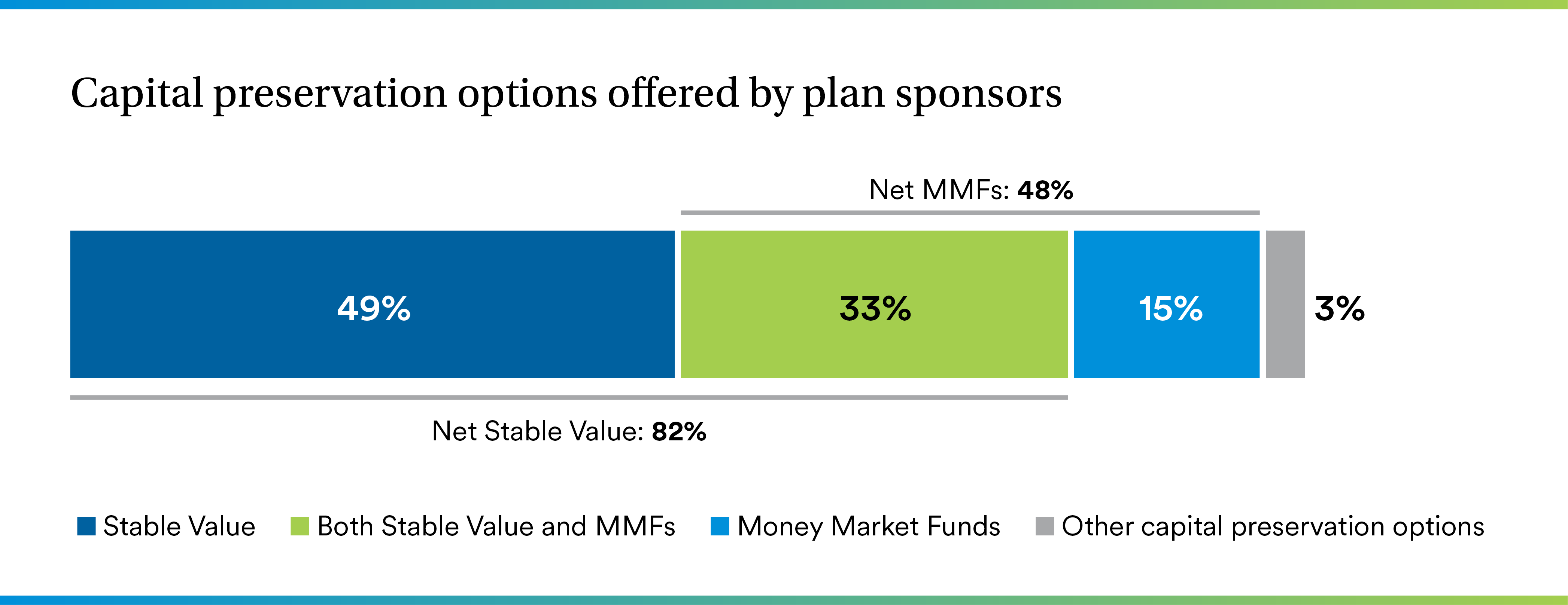

Stable value is widely offered by plan sponsors and has historically delivered higher returns than money market funds, both nominally and in terms of real returns. From 2012 to 2022, stable value returned a nominal 1.99% annualized, while money markets returned 0.50% annualized. Over the same period, stable value’s real returns were –0.31% annualized compared to money market’s –1.75% annualized.

Four things to consider when evaluating a stable value fund

As you are considering which stable value solutions and providers belong in your or your client’s defined contribution plan, there are four main criteria you will want to examine:

The more consistent the performance of a stable value fund, the better. When comparing returns, make sure to look at multiple time periods, including one-, three-, five- and 10-year returns. You will want to see:

· Consistent performance and a long track-record

· No wide fluctuations in crediting rates

· Funds that outperform their peers

· Funds offered by companies with a core competency in stable value funds, such as MetLife

“Long-term performance is very important because it gives you a snapshot into how the fund has performed in various market and interest-rate cycles,” says Curtin. “You want a fund that’s predictable, reliable, and consistent. If a stable value fund portfolio is structured properly, it shouldn’t have wide swings in performance regardless of what happens in the market.”

The net crediting rate is the return that plan participants can expect after expenses.

“It’s the [return] guarantee that’s provided by the insurance company,” says Curtin. “Crediting rates track the general direction of interest rates, but at a lag to the market.”

The net crediting rate is effectively the yield of the underlying portfolio minus expenses along with an amortization of portfolio gains/losses over the duration of the asset portfolio. Look for a crediting rate, or return, that outperforms the median of peer funds with similar portfolio holdings and diversification.

Since stable value funds are typically comprised of bond funds, the market value of the fund’s holdings fluctuates as interest rates rise and fall. Bond funds have an inverse relationship with interest rates. When rates go down, the market value of those securities goes up. And the opposite is true: When rates go up, the value of the securities goes down. In an environment when the Federal Reserve is aggressively raising interest rates, the market value of many stable value funds will be below their book value, or contract value – that is, they will generally follow market interest rate trends, but with a lag.

In general, a market-to-book ratio above 100% is a positive financial sign, as it represents that the market value of the assets is greater than the book/contract value of the assets. However, if the market-to-book ratio dips below 100% due to a rise in interest rates, it also means that the return potential of the fund will trend up over time as a result of future deposits being invested in higher-yielding bonds. In general, a fund’s market-to-book ratio should be evaluated relative to the prevailing market environment, rather than as a stand-alone measure.

“As the Federal Reserve raises rates, the market values of the underlying securities will decrease,” Curtin explains. “If and when the Fed begins to stop raising rates or decrease rates, the market values of the funds will increase as older securities mature and new cash flows are invested at 100% market value.”

As with any investment, fees are another component for review. Just as you would compare the expense ratio of a mutual fund run by a portfolio manager versus a lower-cost exchange traded fund, it’s prudent to compare fees and expenses charged by stable value funds. That said, there is a wide range of fees associated with different stable value solutions. For example, some solutions are invested in an insurers general account (spread products) and do not provide the same level of transparency as other solutions such as separate accounts. A lower fee does not necessarily mean a better outcome for participants. Therefore, any analysis should balance the review of fees versus the NET return to participants. Expenses to scrutinize include the underlying fees charged by the investment managers running the funds as well as the charges levied by the wrap providers, or insurers, who guarantee the fund’s steady returns and protect against losses.

It’s also important to gain a clear understanding of the stable value fund’s contract and product features. For example, make sure the fund’s underlying investments are diversified among different types of bonds, such as U.S. Treasuries, corporate bonds, and mortgage-backed securities, to name a few.

“You want to see if there’s anything in there that would cause volatility to the portfolio,” says Curtin. “You also want to get comfortable with what you’re investing in.”

Another key feature is a stable value fund’s rules related to a plan sponsor liquidating the fund to reinvest elsewhere.

“You want to know not only how you can get into the fund, but how you can get out,” says Curtin.

That’s especially true in rising-rate environments, when the underlying market value of the assets held in many stable value funds is below the contract value. It may be better to choose a fund with a portability feature that allows plan sponsors to remain invested in the fund when moving to a new recordkeeper and simply have the new recordkeeper administer the fund, rather than requiring liquidation and reinvestment ,” says Curtin. “Portability mitigates the majority of downside risk.”

MetLife’s stable value solutions

When evaluating stable value funds, it’s prudent to look for an industry leader that has a proven track record on both the financial and administrative sides of the business.

“You want to look at a company’s history in the asset class,” says Curtin. “Is it a core competency or just a hobby — just another fund they’re looking to add to their lineup?”

MetLife, which has a 45-year history in stable value funds, offers creative and tailored solutions backed by extensive knowledge and experience. Its Stable Value Study is the industry’s go-to source for the latest insights and trends about this popular capital preservation option.

If you’re a plan sponsor or advisor looking for fresh insights about stable value funds or in search of a new provider, reach out to a stable value fund expert at MetLife today.