Tax Implications of Selling a Business

Small business owners may envision turning their firm, practice, or storefront into a sizable payout. If you have a client who is looking to sell their business, they may be counting on the money from that sale to fund the next stage in their life, whether it’s retirement or a second career. Because this sale is a big next step in their financial future, it’s important that they approach the transaction with a tax-minded focus.

The sale of a business, especially when involving a lump sum cash payment, can be a significant taxable event. But there are ways your clients can address their future capital gains and other tax obligations by spreading tax liability over time. Here’s a look at how structured installment sales can help them accomplish their goals.

How Capital Gains Tax Is Calculated for a Business Sale

Most businesses consist of many assets with varying classifications. Every asset needs to be valued when a business owner decides it’s time to sell. The valuations must be recorded, as they will need to be accounted for during the transaction.

Each asset is also classified into categories including:

- Capital assets

- Depreciable property that was used in the business

- Property held for sale to customers (such as inventory or stock in trade)

The gain or loss of each asset will be figured individually in part based on the classification type for tax purposes. For example, when a capital asset is sold, it either results in a capital gain or a capital loss. But when inventory is sold, the sale results in ordinary income or loss.

Your client’s tax liability after selling a business will depend on the type of assets sold and the form of sale. If they receive the business sale proceeds in one lump sum, they might face not only capital gains tax but also significant net investment income taxes, or NIIT, and state income taxes, which are typically due in the year of the sale.

In general, business owners can expect the capital gains tax rate from a business sale to range between 0% and 20% of the profit. If your client’s income exceeds certain levels, the NIIT would add 3.8% in tax as well.*

Can Your Clients Use a Structured Installment Sale When Selling a Business?

Certain business sale transactions can be executed as a structured installment sale, rather than a lump sum sale. When using this method, all parties agree to installment payments for a stated number of years as a condition of the sale. The periodic payments are then made by an insurer.

A structured installment sale may offer beneficial tax treatment, in that the taxes are paid as the installment payments are received rather than being paid entirely in the year of disposition. This allows sellers to defer their capital gains taxes and other tax obligations over a longer period.

Read a small business case example of a structured installment sale

Tax Considerations of an Installment Sale

There are certain tax rules, as outlined by Sections 453 and 453B of the Internal Revenue Code, that apply specifically to installment sales.

Generally, business owners can only use an installment sale for capital assets that have been held for more than a year. If a business has inventory to sell, those assets do not qualify for installment sale treatment. Taxes must be paid on these types of business assets in the same year the business is sold, even if payments are received in later years.

Sellers are also unable to use the installment method to report gains from the sale of stocks and securities traded on an established securities market. The seller must report any portion of the capital gain from the sale of depreciable assets as ordinary income under the depreciation recapture rules in the year of the sale.

If the business and its assets are being sold at a loss, the installment method rules do not apply.

The Benefits of a Structured Installment Sale

A structured installment sale offers sellers the distinct advantage of incorporating an insurance company into the equation.

Insurance companies are highly regulated and have strict reserve requirements to prevent insolvency. They also typically have strong financial strength ratings from leading credit rating agencies, which demonstrates their ability to meet future financial obligations.

With a structured installment sale, the buyer assigns the payments to the insurer’s assignment company.3 The assignment company, in turn, agrees to take on the obligation and will use the lump sum provided by the buyer to purchase an annuity contract matching the specified periodic payment obligation. The insurance company will then issue the annuity to the assignment company and distribute future payments to the seller according to the schedule originally determined in the purchase and sale agreement. This way, the seller has the assurance of receiving future payments (which can serve as income for retirement) from a highly-rated insurance company.1

Examples of Using a Structured Installment in a Business Sale

To see how a structured installment sale can benefit business owners, let’s look at an example:

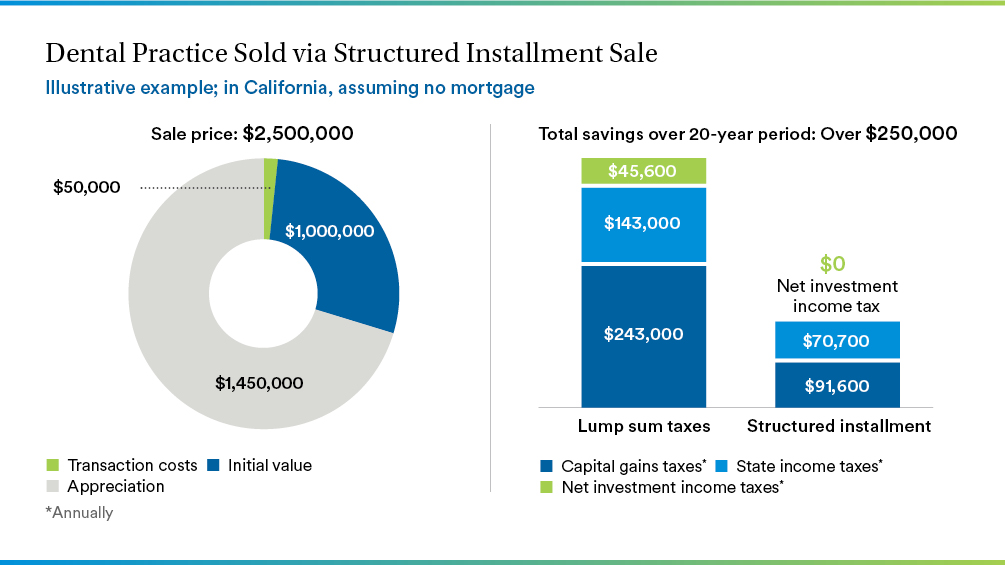

Jose is a 55-year-old dentist and business owner in California who, for many years, owned a major dental practice. He’s decided to sell his practice to fund the next phase in his life, which is retirement.

The dental practice is in good shape but needs a refreshed marketing strategy and capital improvements to bring the next generation of customers. Selling the dental practice now will help Jose avoid an outlay of capital and help reduce his responsibilities in retirement.

After putting his practice on the market, he accepts an offer of $2,500,000. The dental practice’s adjusted basis is $1,000,000 and the selling expenses associated with the transaction are $50,000 resulting in a gain of $1,450,000. The dental practice’s property is not subject to a mortgage.

During the sales process, Jose consulted with his legal and tax advisors who advised that he should receive the proceeds in a structured installment sale. This was the best option for Jose because he didn’t need the full sale proceeds immediately, and this structure would defer and reduce associated capital gain, NIIT, and state income taxes. In cooperation with the buyer, he structures $2,500,000 of the sale proceeds to be payable as follows: $191,755 payable in equal amounts for 20 years per the Purchase and Sale Agreement.

How a Structured Installment Sale Can Make Your Offer More Attractive

Because of the potential tax benefits to the seller, a buyer interested in purchasing a business may be able to make a more attractive offer by utilizing a structured installment sale.

Using the example shared above, here’s how Jose’s tax obligation would differ by accepting installment payments over a single sum.

If Jose had received the proceeds in full at the time of the sale, he would have to pay close to $239,493 in federal capital gain taxes (at a marginal 20% federal capital gains rate), as well as about another $45,600 due to the 3.8% NIIT. Additionally, since Jose is a resident of California which has graduated tax rates depending on income level, he would be subject to higher rates resulting in over $141,000 of associated state income taxes.

Since Jose has chosen an offer that uses a structured installment sale, he will pay approximately $5,819 of federal capital gains taxes annually over the 20 years (taking advantage of the 0% and 15% capital gains tax rates).

In addition, by spreading the gain over a period of years, he will avoid net investment income taxes altogether. His associated state income taxes would be about $6,061 annually. This results in capital gains, NIIT, and state income tax savings of over $188,000.*2

His savings is due to the tax rules applicable to installment sales which generally provide that each installment payment, which comprises a return of basis, capital gain and interest (with the interest taxed as ordinary income), will be taxable over time when paid to the seller. As a result, Jose was able to manage his annual taxable income and leverage lower tax brackets.

Because business owners often rely on the sale of their business to fund their retirement, the opportunity to pocket more profit and defer and reduce tax obligations can make an offer much more attractive to the seller.

*Rates are subject to change as of July 1, 2025.

Finding the Right Insurer

Working with your client and their tax and legal advisors to determine whether a structured installment sale is in your client’s best interest is an important first step, but choosing the right insurance company to entrust is critical. This sale is instrumental in funding the seller’s retirement or other future financial goals, and they want to be confident that they’ll receive future payments.

To do this, try to help them find a company that has a proven track record of making long-term annuity payouts — and is able to withstand market volatility and economic turmoil.

You can also ask for the insurance company’s credit ratings or look for them on the company website. Credit ratings are strong indicators of an insurance company’s financial stability. There are four major insurance company rating agencies: A.M. Best, Moody’s, Standard & Poor’s, and Fitch. Because each agency has its own rating scale, the same insurance company could receive different ratings from the various agencies. Make sure to visit the rating companies’ websites to ensure you understand their rating scales.

Metropolitan Tower Life (Met Tower Life) is a leader in the insurance space and structured settlement market — holding an A+ rating from A.M. Best, an Aa3 rating with Moody’s, an AA- with Fitch, and an AA- with Standard & Poor’s. Backed by MetLife’s robust resources and longstanding history of insurance excellence, Met Tower Life has proudly served as a trustworthy and credible insurance provider for many business owners.1

For more information, please contact:

Paul Marshall - Sales Director

pmarshall1@metlife.com

Philippe Petit - Sales Director

ppetit@metlife.com