Structured Installment Sale

.

What is a Structured Installment Sale?

A Structured Installment Sale (SIS) is a tax-deferral solution designed to help manage potentially large capital gains tax from the sale of an asset.1 Rather than recognizing the entire gain in the year of sale, the Seller can choose how much of the proceeds to receive upfront and how much the Seller would like to receive in the future. The payment stream can accommodate more immediate needs, under the traditional SIS, or help plan for the longer term, like retirement, with the SIS Flex Agreement (SIS-FA).2,3

Case Example Video

Discover how a tax-efficient, structured installment sale can benefit both buyer and seller in a sale of a property or business.

How does a Structured Installment Sale work?

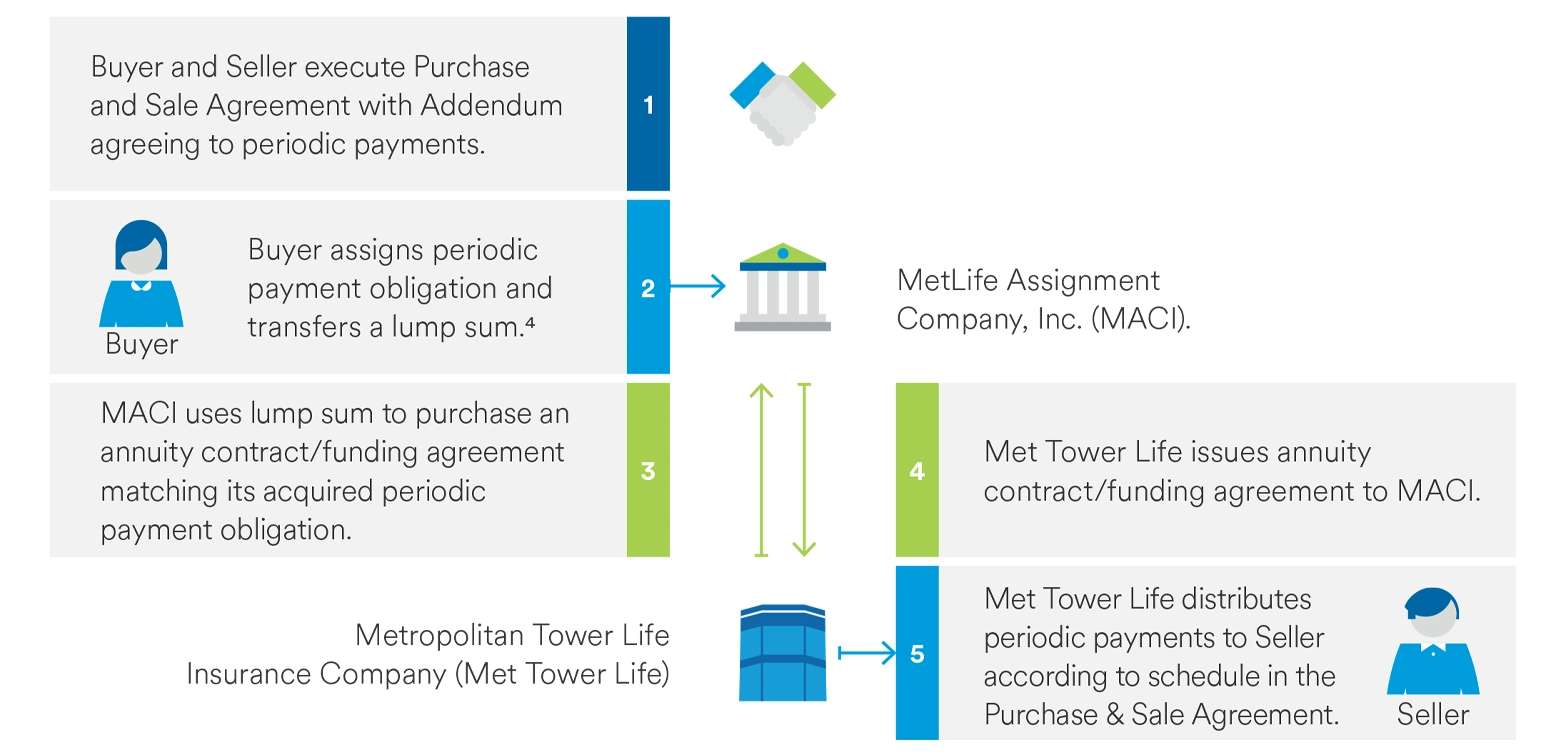

Instead of receiving one lump sum, the Buyer and Seller agree to periodic payments for a stated number of years as a condition of the property and/or business sale. The periodic payment obligation is then transferred to MetLife Assignment Company, Inc. (MACI) by the Buyer, who pays the full premium to cover the payments. MACI purchases an annuity/funding agreement from Metropolitan Tower Life Insurance Company (Met Tower Life). Met Tower Life then issues the scheduled payments to the Seller on behalf of MACI. Both entities are wholly owned, U.S. based subsidiaries of MetLife, Inc. and, as such provide great confidence for all parties.4

DISCOVER

Why choose a structured installment sale

Selling a real estate property or business can have significant tax implications. When a seller receives their sales proceeds in a lump sum, they might face not only capital gains taxes, but also net investment income taxes and state income taxes, which are due in the year of the sale.1

Our Structured Installment Sale solution can help reduce taxes on the proceeds, while providing a stream of guaranteed income over time to help secure their financial future.1

Tax Implications of Selling Real Estate with a Structured Installment Sale

A structured installment sale (SIS) allows the seller of real estate, property, or agricultural land to be paid in future installments over a period of time, rather than a one-time lump sum. Because taxes will then be paid based on the income received each year, this structure helps the seller defer their capital gains tax and potentially decrease the overall tax liability on the sale.

Tax Implications of Selling a Business with a Structured Installment Sale

A structured installment sale (SIS) may offer beneficial tax treatment when selling a business because the taxes are paid as installment payments over a period of time, rather than being paid entirely in the year the business is sold. This allows sellers to defer and potentially reduce their capital gains taxes and other tax obligations by spreading the payments out over a longer period.

What are the advantages of a Structured Installment Sale?

Tax Benefits1

Deferral and potential reduction of capital gains tax, Net Investment Income Tax (NIIT) & state income tax

Guaranteed Income

Conversion of proceeds into a guaranteed income stream, immune to market volatility and performance2

Flexibility

Tailor payment start dates to meet individual needs6

Trustworthy

Payments secured by a financially sound and trusted company5

Explore potential outcomes with Structured Installment Sales

CASE STUDIES AND RESOURCES

Case Study: Small Business Sale

Read Jose's case on selling a dental practice. Learn how an SIS helped him defer capital gains tax and turned the proceeds into a guaranteed income stream.

Case Study: Real Estate Sale

Read Mary's case on selling a real estate property. Learn how an SIS helped her defer capital gains tax and turned the proceeds into a guaranteed income stream.

Whitepaper: Structuring an Installment Sale

Explore the mechanics of a Structured Installment Sale and how it works for business and real estate sales including the associated tax benefits.

Accounting Today: Tax Strategies for SIS

Explore the strategic ways to help minimize capital gains taxes when selling a business or property with a Structured Installment Sale.

Kiplinger: Benefits for Buyers and Sellers with SIS

Find out how structured installment sales can help sellers defer taxes while generating guaranteed retirement income.

Whitepaper: SIS Competing Product Types

While structured installment sales offer a tax-efficient way to defer capital gains taxes, learn about the alternative products available that may suit different financial needs and goals.

FAQs

A type of non-qualified assignment designed for property and business sales to transfer periodic payment obligations to an assignment company where the Seller will receive at least one payment after the tax yearin which the sale occurs. This solution is designed for property and business sales that are eligible for the Installment Method under Internal Revenue Code Section 453.1

Process:

- Buyer and Seller execute Purchase and Sale Agreement with Addendum agreeing to periodic payments

- Buyer assigns periodic payment obligation and pays a single sum to MetLife Assignment Company, Inc. (MACI)4

- MACI uses the single sum to purchase an annuity contract/funding agreement matching the acquired periodic payment obligation

- Metropolitan Tower Life Insurance Company (Met Tower Life) issues annuity contract/funding agreement to MACI

- Met Tower Life distributes periodic payments to Seller accordingly

- Disposition of inventory

- Dealer disposition of real and personal property with certain exceptions as provided in IRC Section 4531

- Disposition of stock and securities traded on an established market

- Portion of the gain attributable to depreciation recapture taken on real or personal property

- Disposition of depreciable property between related persons with certain exceptions as provided in IRC Section 4531

Always consult your independent tax advisors to review eligibility under IRC 4531.

In general, if your seller’s installment sale obligations (i.e. payments that you are owed) are greater than $5M, the IRS imposes an interest charge. Please refer to IRC Section 453A(a)(1)1. Exceptions to this rule include:

- Personal use property and

- Trade or business, related to farming

Always consult your independent tax advisors to review eligibility under IRC 4531.

Periodic payments must be made for the benefit of the individual or the entity that is named as a party to the sale. Outside of issuing payments directly to the named individual or entity, acceptable payees may also include trusts, businesses, or corporations but home office approval is required.

With the traditional SIS, periodic payments must start immediately (within one year of purchase date).

With the SIS-FA, there is flexibility in how the periodic payments can be issued. Payments may be issued in the form of a single lump sum or a series of payments. Annual increases are also offered.2,3

No, periodic payments cannot be life-contingent. Any remaining unpaid guaranteed payment(s) will continue to the beneficiary (either named beneficiary or estate). If elected at the time of assignment, payments may be commuted upon death for the traditional SIS or follow the accelerated benefit event for the SIS-FA.2,3

No.

In general, each payment on an installment sale consists of the following three parts:

- Interest income

- Return of your adjusted basis in the property

- Gain on the sale

1099-B Proceeds from Brokers and Barter Exchange Transactions. Met Tower Life completes sections 1a-1d, 4 and 6. Proceeds are reported on a gross proceeds basis on annual installment payments.

Seller/Payee uses Form 6252 to report income from an installment sale on the installment method.

Advantages of Working with Us

Proven Industry Leadership

More than 40 years of consistent market leadership and #1 in sales in the structured settlements industry.7

Financial Strength & Stability

Our financial strength ratings are among the highest in the industry, ensuring long-term payment security.5

Customized, Flexible Solutions

Trusted Expertise and Guidance

Experts delivering clear, compassionate guidance and industry leadership.

Solutions-Focused Partnership

Streamlined processes, innovative tools, and collaborative support that help make every step of the process easier.

Commitment to Claimant Well-Being

Products designed to support claimants’ long-term needs while delivering consistent, reliable income for the future.

Meet The Team

When you partner with us, you are choosing a leader who will be with you every step of the way and can provide a steady and reliable income stream — both now and in the future.