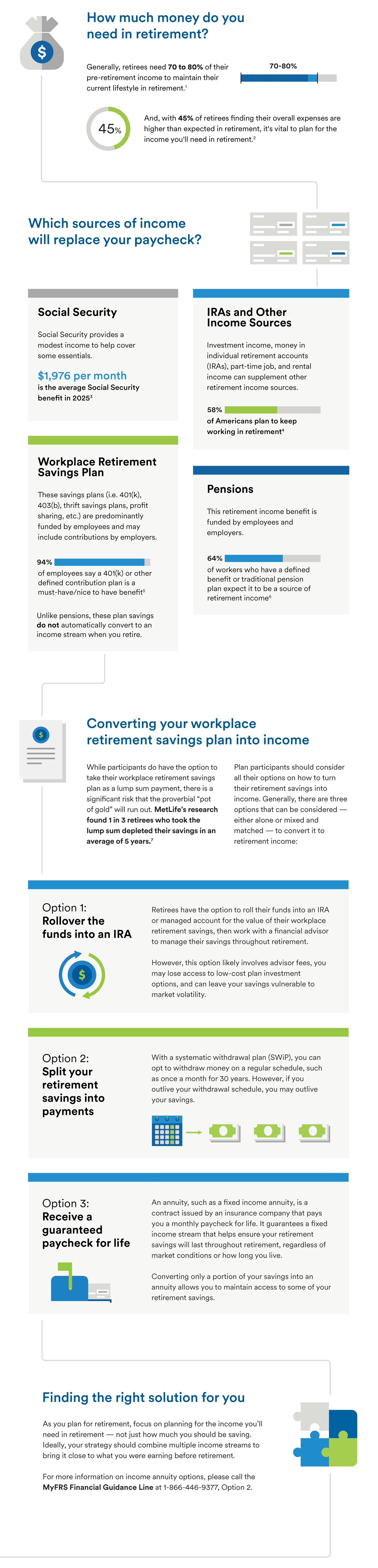

1. Top 10 Ways to Prepare for Retirement, U.S. Department of Labor, September 2023.

2. 2022 Spending in Retirement Survey: Understanding the Pandemic’s Impact, EBRI, October 2022.

3. Understanding the Benefits, Social Security Administration, January 2024.

4. Over Half of Americans Plan To Work in Retirement: Here Are the Best Options, Nasdaq, March 2023.

5. MetLife's Employee Benefit Trends Study, 2024.

6. Retirement Confidence Survey, Employee Benefit Research Institute, 2023.

7. MetLife's Paycheck or Pot of Gold Study, 2022.

Group annuity contracts are issued through Metropolitan Tower Life Insurance Company (MTL) or Metropolitan Life Insurance Company (MLIC). Like most group annuity contracts, MTL and MLIC group annuities contain certain limitations, exclusions and terms for keeping them in force. MTL and MLIC annuity products may not be available in all states. Contact your MetLife representative for more information.